Using AVS to Reduce Chargebacks and Strengthen Your Defense

Chargebacks are one of the more frustrating parts of running an operation. They’re time-consuming, expensive, and in a lot of cases, feel completely disconnected from what happened on the trip.

While there’s no way to eliminate chargebacks entirely, there are ways to reduce how often they happen and improve your chances of winning when they do.

One of the most important factors in that process, and one that often gets overlooked, is AVS (Address Verification Service).

Understanding Credit Card Chargebacks

A chargeback happens when a client disputes a transaction with their bank instead of working directly with you. Common reasons include:

- Fraud or unauthorized use

- Dissatisfaction with the service

- Claims that the service was not provided

- Billing disputes

Once a chargeback is filed, the focus shifts. It’s no longer just about what happened operationally. It’s about what you can prove.

How LA Pay Helps Prevent Chargebacks

Using a secure and reliable payment processor is your first line of defense.

LA Pay is designed to help you collect the information needed to both validate a transaction upfront and defend it later if needed. LA Pay requires:

- CVV Code

- ZIP Code

- Building number of the street address

This isn’t just for compliance. It directly impacts how the transaction is evaluated if it’s ever disputed.

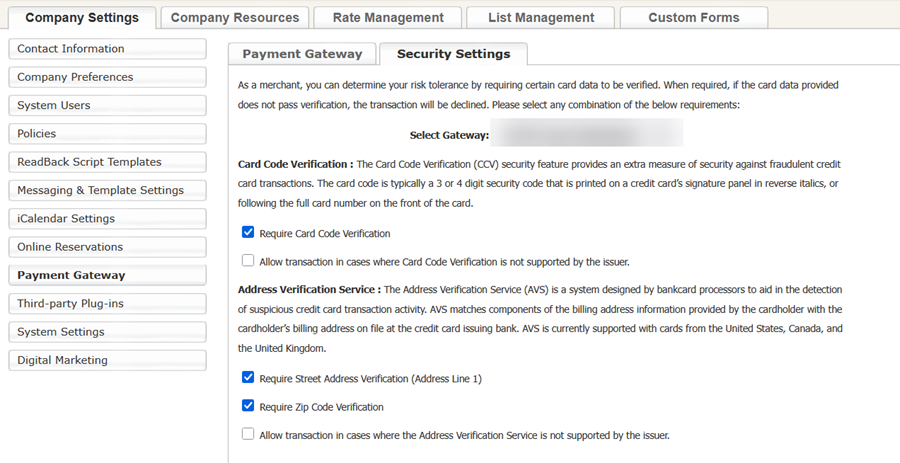

If you’re currently using LA Pay, you can review and adjust your AVS and card validation settings directly in your system.

To access these settings:

- Click the "My Office" icon in the navigation bar

- Select "Company Settings"

- Open the "Payment Gateway" tab

- Navigate to "Security Settings"

From here, you can configure requirements such as:

- Street address (Address Line 1) verification

- ZIP code verification

- CVV (card code) verification

These settings allow you to align your payment validation process with your risk tolerance. Requiring stricter validation can help reduce fraudulent transactions, but may also decline legitimate cards in some cases, so it’s important to find the right balance for your operation.

NOTE: AVS Is Not Just a Checkbox

AVS (Address Verification Service) compares the billing information provided by the client with what the issuing bank has on file. A full match (street number + ZIP code) helps support your case. It shows the person making the payment had access to the cardholder’s billing information.

If neither the address nor ZIP code matches, the transaction is considered high risk. At that point, it’s not about whether you provided the service correctly. It’s about whether the bank believes the transaction was authorized. Industry data suggests that merchant win rates in these cases can fall to around 9%, meaning most disputes are decided in favor of the cardholder.

If you’re using LA Pay, you can also review AVS response codes directly in Merchant Track under the transaction details. These responses are typically shown as letter codes and indicate how closely the billing information matches what the issuing bank has on file.

Some of the more common AVS response codes you may see include:

- M – Full match (street number and ZIP code both match)

- Z – ZIP code matches, but street number does not

- A – Street number matches, but ZIP code does not

- N – No match (neither street number nor ZIP code matches)

- U – Address information unavailable or not supported by the issuer

- R – Retry (issuer system unavailable, verification not completed)

From an operational standpoint:

- M (Full Match) is your strongest position in a dispute and generally indicates lower risk

- Z or A (Partial Match) should be reviewed more closely, especially for higher-value trips

- N (No Match) carries significant risk and a much lower likelihood of winning a chargeback

- U or R are inconclusive and may require additional verification before proceeding

This gives you a quick way to confirm whether a transaction actually passed AVS or just went through, which becomes important if that transaction is ever disputed.

Using Payment Requests and “Request a Card” to Reduce Liability

Card-not-present transactions, especially when card details are taken over the phone, carry higher risk by default.

Even when everything seems legitimate, you’re relying on information being relayed to you and manually entered into the system. That creates more room for error and makes it harder to defend the transaction later if it’s disputed.

This is where Request a Payment and Request a Card can make a meaningful difference. Instead of collecting card details directly, you can send a secure link to the client and have them enter their own payment information. In both cases, the cardholder enters their billing address, ZIP code, and CVV through a secure, encrypted form rather than over the phone.

NOTE: These tools don’t eliminate chargebacks, but they help demonstrate that the cardholder actively participated in the payment process, which can strengthen your position in a dispute.

Further Strengthening Your Chargeback Protection

For additional protection, tools like Contract & Credit Card Capture allow you to:

- Collect full credit card details

- Request identity validation

- Obtain acceptance of terms

- Secure a digital signature

This adds another layer of documentation that can support you if a transaction is disputed.

If you’d like to learn more about LA Pay’s features or review your current setup, reach out to Support. If you’re interested in getting started with LA Pay, you can contact Sales at 972-701-8887 (Option 1).

Recent Posts

July Product Release Update

Sunday July 5, 2026